|

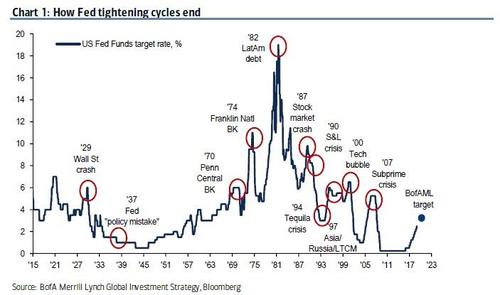

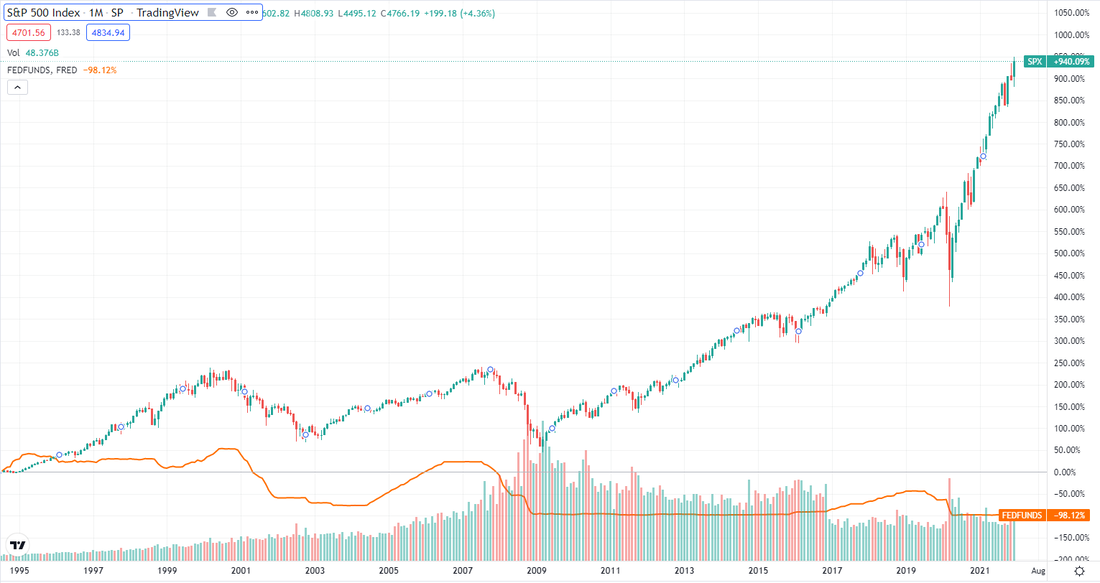

Last week was a very busy week! Frustratingly, it ended pretty much flat after the mother of all short covering rallies in the closing minutes of Friday’s trading session. I say "frustratingly" because I held onto more growth-oriented positions until Friday waiting on a bounce. When it did not appear the bounce would occur at these levels (see March 2020 decline for reference), I decided I had better cut bait and sell out of many of them. Not ideal timing, but I did add back a little of that exposure on Monday for a trade post the short covering rally. So where do we go from here? Great question! Over the weekend, I listened to advisors and managers make the case for the Fed to capitulate and markets to reverse higher all the way to the opposite extreme of the Fed is trying to crash the markets. I honestly can say there is no general consensus! So, we turn to the charts, they can sometimes help when the markets appear confused and there is no clear path forward.  Above is a 4-hour chart of the S&P 500 Index. What you will notice on this chart is the market is bouncing but within what we call a Bear Flag (the area between the two dotted back lines). What does a Bear Flag typically mean? It usually is a continuation pattern that in this case could resolve itself lower. If we took the recent all-time high of 4,818.62 and subtracted the recent low of 4,222.62, we get 596 S&P 500 points or roughly 600 if we round. If we then measure 600 points lower from the top of the Bear Flag pattern (estimated at 4,500), that gives us a rough target of 3,900 on the S&P 500 or another 13% lower. Top to bottom this would give us a 19-20% correction. I think this is a real probability in the coming weeks. Now the disclaimer – this is just a guess. Anything could happen from the Fed getting dovish to seven rate hikes, as Bank of America is now forecasting over the next two years. I will say this, the next four months will likely be very volatile! I expect there is a great deal of pressure on the Fed to deal with inflation, even if it ends up being transitory. This could mean they lean towards a larger number of rate increases and risk pushing the economy to the brink or into recession. It will be a delicate balancing act; one the Fed usually gets wrong historically as you can see below!

0 Comments

Summary

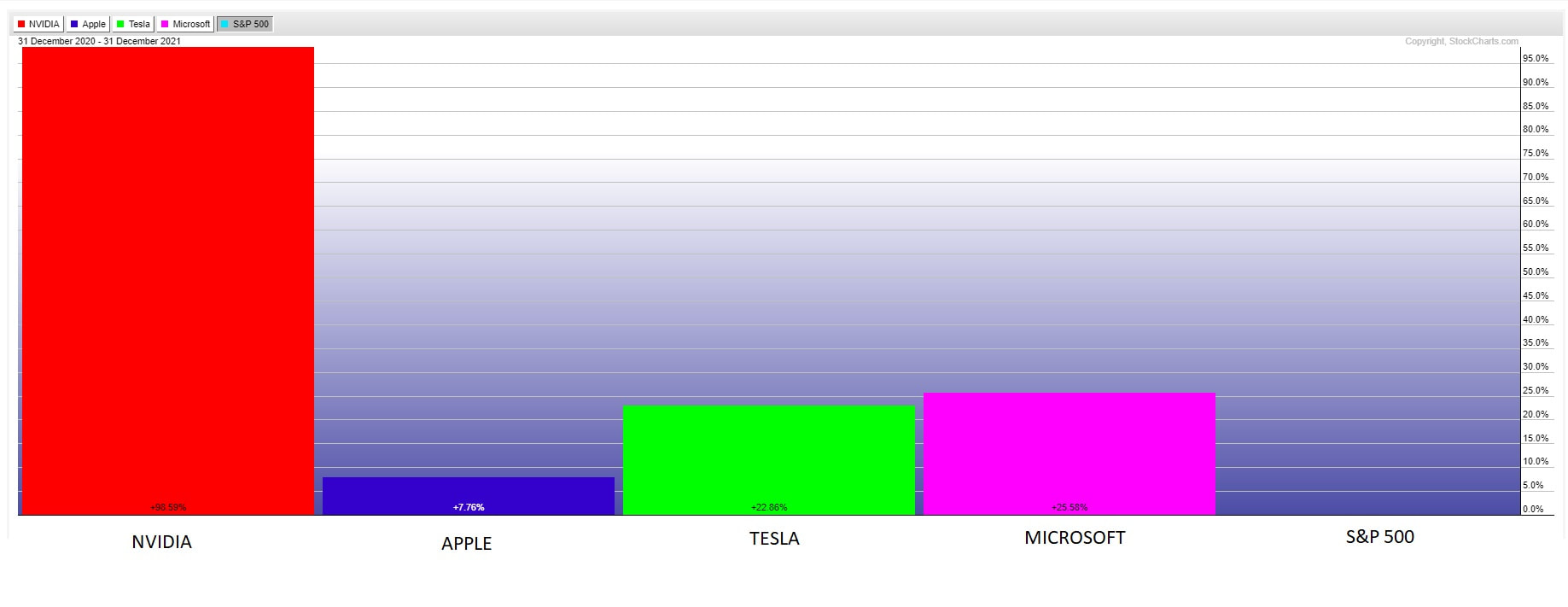

The Year That Was Happy New Year to all our readers! 2021 was a fabulous year if you invested almost entirely in names, such as Apple, Microsoft, Nvidia and Tesla in 2021! Here is their performance relative to the S&P 500 index.  You can see that they all outperformed the S&P 500 index for the year on a relative basis. Otherwise, the S&P 500 index (in red) ruled the day, because of those four names, and an end of the year rotating bear market in many other names that wreaked havoc in other indexes.  The Year Ahead (What is to Come – Possibly) 2022 stands to be a more challenging year than 2021! However, let’s remember a couple of things that recent history has taught us.

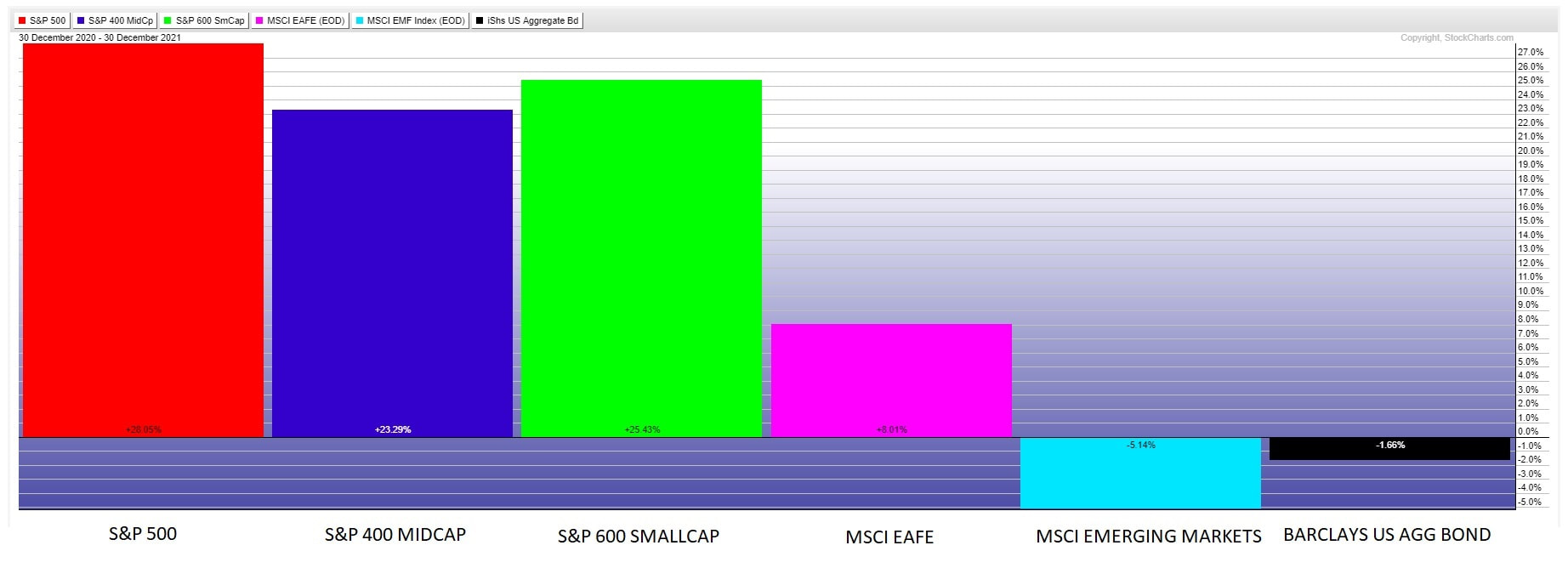

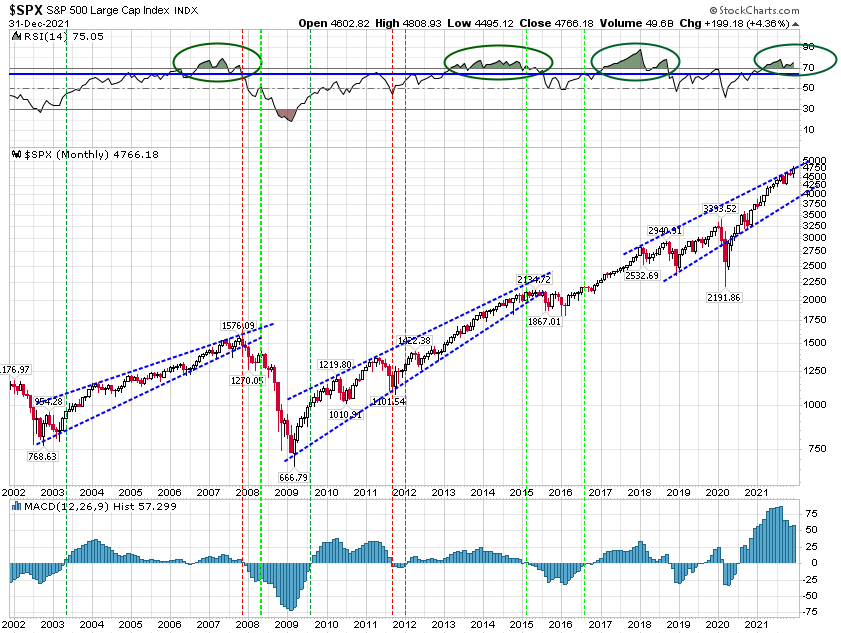

Here is the U.S., the Federal Reserve has started to taper the purchase of treasury securities and plans to raise the Fed Fund rate starting in mid-2022, which would usually have the effect of lowering demand for our U.S. treasuries and raising interest rates. This is exactly what has happened with short-dated bonds, but longer dated bonds are still trading in a consolidation range, possibly signaling that the bond market thinks the Fed is too late and that inflation is already moderating (remember deflation usually follows inflation). The increase in the rates of short-term bonds is why the Barclay’s Aggregate Bond Index lost -1.77% in 2021. Despite the constant negative news and bear market predictions, we think there is a decent chance that the overall market continue higher. Here is why? The S&P 500 index RSI is trending above 70 (top indicator, circled in green). When this indicator is above 70, it tends to stay above for 14-15 months on average and lead to strong gains of more than 24% on average. Given the current run above 70 on the RSI, we can project another 3-4 months of positive to sideways market returns and +3.33% based on the historical averages. This is the average, and it should be noted that the longest such run since 1997 was 27 months in 2013-2015 and this resulted in a market gain of more than 39.1% over that period. We believe it is possible, we stay above the 70 RSI mark for much of 2022. Of course, that is just a guess and certainly past performance is never a guarantee of future performance!  The other reason? Fed tapering and rate increases don’t cause Bear Markets. Policy errors, such as raising rates too much or too fast, cause Bear Markets. As you can see below, when the U.S. Federal Reserve has raised interest rates in the past (the orange line), the S&P 500 index has continued to climb. It is only when rates went too far, and the Fed starts to flatten or reverse rate hikes that the market falls. If you look at the three historical periods of rate increases, below, you had roughly a year in which the markets rose, and rates also increased in each case. The Fed does not plan to start raising rates until mid-2022 and this is why we think 2022 could be volatile but generally positive return year.  Now the disclaimer. Not every index may rise. Many such as non-U.S. markets could struggle over the entire year. To us it looks like non-U.S. markets are oversold, could rally higher and then resume their struggles, but this is pretty tough to forecast.

We are still advocates of broadening diversification, but 2022 could prove another year of narrow leadership. It might not be until 2023 that a Central Bank policy error occurs, and diversification finally works to narrow losses, but we can save that for another post. Disclaimers/Definitions This information is for educational purposes only. Please do not rely on this forecast nor trade based on it. Past performance is not indicative of future performance. The S&P 500 Price Index is a capitalization weighted index of the 500 leading companies from leading industries of the U.S. economy. It represents a broad cross-section of the U.S. equity market, including stocks traded on the NYSE, Amex, and Nasdaq. The S&P MidCap 400 Index, more commonly known as the S&P 400, is a stock market index from S&P Dow Jones Indices. The index serves as a barometer for the U.S. mid-cap equities sector and is the most widely followed mid-cap index. To be included in the index, a stock must have an unadjusted total market capitalization that ranges from $3.2 billion to $9.8 billion at the time of addition to the index. The S&P SmallCap 600 Index (S&P 600) is a stock market index established by Standard & Poor's. It covers roughly the small-cap range of American stocks, using a capitalization-weighted index. To be included in the index, a stock must have a total market capitalization that ranges from $700 million to $3.2 billion at the time of addition to the index. As of 31 December 2020, the index's median market cap was $1.26 billion and covered roughly three percent of the total US stock market. These small cap stocks cover a narrower range of capitalization than the companies covered by the Russell 2000 Smallcap index which range from $169 million to $4 billion. The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. The Index is available for a number of regions, market segments/sizes and covers approximately 85% of the free float-adjusted market capitalization in each of the 21 countries. The MSCI Emerging Markets Index reflects the performance of large-cap and medium-cap companies in 27 nations. All are defined as emerging markets. That is, their economies or some sectors of their economies are seen to be rapidly expanding and engaging aggressively with global markets. The MSCI Emerging Markets Index currently includes the stocks of companies based in Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates. The iShares Core U.S. Aggregate Bond ETF seeks to track the investment results of an index composed of the total U.S. investment-grade bond market. The federal funds rate refers to the target interest rate set by the Federal Open Market Committee (FOMC). This target is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. The FOMC, which is the making body of the Federal Reserve System, meets eight times a year to set the target federal funds rate, which is part of its monetary policy. This is used to help promote economic growth. It seems today that there is a law firm on every corner and at every social event you can’t reach out your arm in any direction without hitting an attorney. I believe the only more prevalent professions seem to be financial advisors and real estate agents. I frequently joke that I can go to any event, throw my pen indiscriminately and hit another financial advisor. This may not be exactly factual, but it is probably not too far from the truth given the extended term of this current bull market!  How about you? Have you ever watched late night or free over the air waves digital television? If you have you have probably witnessed the continuous barrage of law firm commercials claiming they are serving your rights and can get you the “settlement you deserve.” If you had just landed here from another planet, you would assume that all earthlings do is sue each other!

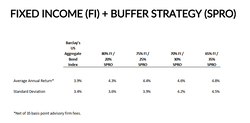

Surprisingly, the National Center for State Courts (NCSC) analyzed civil lawsuit data for 26 states. The NCSC found that tort cases—those involving an injured party seeking damages from a negligent party—made up less than 3% of all civil cases in 13 of those states, 3-5% of civil cases in 8 states, and 5-8.2% of civil cases in 5 states. Moreover, product liability cases and medical malpractice claims made up less than 1% of civil cases. The majority of civil caseload is made up of contract and small claims cases. They also found that tort cases in the U.S. are on the decline. In 13 states, tort filings decreased by 25% from 1999 to 2008 Does this mean you can live recklessly, party like it’s 1999 and ignore the risk of lawsuits? Obviously, the answer is “no”, especially if you are affluent! There are still over 286,289 civil case filings every year in the U.S. according to 2019 U.S. District Court records and that number is growing at a 3% rate annually. That is a large number of civil lawsuits to be sure! There is no statistic for this, but I would wager that most of such civil suits target the wealthy over the poor since they are the ones with the assets and deeper pockets. So, what is the solution? Should you cower in fear in the corner? Move to the most isolated place on earth and hope no one finds you? Obviously not! The answer is to arrange your affairs in such a way as to minimize your exposure. We recently landed a new client who owned substantial real estate holdings. This client had no liability nor property insurance on any of their real estate holdings. These properties were owned by them individually and not in any entities. I should also mention this couple had substantial other assets and made a significant income from their business interests. However, they had failed to stand back and see the impact of that income on their net worth and the amount of assets that were now at risk. It was no longer just a given property that would be at risk but potentially the entire portfolio, their income, and other assets. In talking with them, we discussed the possibility of loss from fire or other hazards on their rental properties and they were very comfortable with such risk. However, when we reviewed their current structure, we determined that we could greatly reduce the risk of a frivolous lawsuit just by arrange the properties differently and looking at purchasing liability coverage on the portfolio of such holdings. We are currently working with their legal counsel to put each property in a separate limited liability company (LLC) with 100% ownership by a holding company. We are also setting up a separate property management entity to oversee each property’s management, collections, and payment of expenses. Yes, this structure will cost a few dollars to set up and it will increase their annual costs some, but it will also significantly reduce the chance that a frivolous lawsuit from one of their properties, tenants, or visitors to the properties, impacts their other business income or asset holdings. By the way, this all came about because the underlying client asked if we could help them with the accounting for their real estate properties. When we first looked at the bigger picture, we noticed the larger risk and opportunity to help reduce this risk. The question I then have for you is “how can we help you today?” We are not just an investment advisory firm, but a complete family office solution for affluent families! Maybe it would be worth exploring how we can simplify your life and allow you to pass more to your heirs, while minimizing the impact that creditors and your dear broke Uncle Sam has on your assets. Why not connect with us today?  I get asked frequently "how can I find a better yield on my cash deposits?" The answer - "that one is a hard one! How much risk are you willing to take to get higher yields?" Their response is usually "no more than I am taking now at my local bank." The problem is that the Federal Reserve (the "Fed") has those seeking yield in between the proverbial rock and a hard place. The Fed policies of buying outstanding debt (i.e., quantitative easing) to keep rates on treasuries low and, thereby stimulate economic growth, have really hurt savers. They have also forced investors to take greater risk to earn higher investment returns so they at least keep up with inflation. This in turn has created bubbles in many asset classes that have significantly stretched historical valuations and investment risk metrics. So what is a yield starved investor to do? Today we will explore a handful of options. However, I don't think any of these options is a singular answer. Instead a diversified approach may be your best option in this challenging environment! 1. Crypto Stable Coins I mentioned crypto stable coins like Tether, USDC and UST in a recent post called Miscellany. For instance, I converted U.S. dollars into USDC stable coin and then put it on deposit at several crypto banks and now earn north of 8% on those funds. The downside? Crypto is lightly regulated and the SEC is now stepping up it's reviews of stable coin providers and their underlying reserves. In my personal case, I didn't put more than I could afford to lose in stable coin and I split it up amongst several U.S. based crypto banks. You can find out more about this option in an article entitled What are Stablecoins and Why Invest in Them? 2. High Dividend Stocks There are high dividend stocks and stock funds such as Amplify's High Income ETF(symbol YYY) which currently yields 9.04%, according to ETF database. The problem with high dividend stocks are 1) they have high dividends usually due to a price decline or a high degree of investment risk and 2) if markets go down, the yield will rise but any gains here will be offset by unrealized losses in the underlying stock or ETF. Take a look here at YYY (red line) vs. the S&P 500 ETF (SPY) (blue line).  Wouldn't you rather have had the return of the S&P 500 when it appears you are taking a lot of risk in the Amplify High Income ETF based purely on comparing the periods of market decline for both securities? A solution here might be to actively trade or apply a trading methodology to ETF, but even so you could do that to the S&P 500 as well and earn a higher overall return. 3. Total Return Strategies With total return strategies, you are not looking for yield, but a greater overall portfolio return. Instead of distributing income to support your lifestyle, you periodically raise some cash and make distributions from principal. We recently released a total return strategy for enhancing cash returns. It allocates between 65-80% of the portfolio assets to fixed income ETFs that are chosen based on their yield adjusted duration. The idea here is to get as much yield per unit of duration (e.g. a measure of a bond's or fixed income portfolio's price sensitivity to interest rate changes) as possible. It pairs that with a diversified portfolio of buffered ETFs where each position has both a known floor (loss) and capped upside. Essentially giving up some potential upside for a lower downside. The result:  Disclosure, these results above are ALL back tested using the CBOE S&P 500 Buffer Protect Index Balanced Series plus the Barclay's Aggregate Bond Index. This former index may not exactly match the diversified index of buffered ETFs. Past performance is not indicative of future performance.

Now that we have that out of the way, you can see that based on this historical data since 2006, we where able to enhance overall total returns with less risk (i.e., standard deviation) at least in back-testing. 4. High Yield Teaser Rates The final area where you can get enhanced yields in from internet firms offering teaser rates for new customers. Bankrate.com has a whole list of such firms, mainly internet banks offering yields of around 50 basis points at present. The difficulty we have found with such rates are they are only available to individuals, not businesses and each has minimum deposit amounts and restrictions. 5. A Diversified Bond Portfolio One final option might be just a plain old fixed income portfolio. With the right allocation, you can get yields north of 2.5%+ and durations as low as 3.08. We do this for clients and also change positioning from time to time to minimize downside when rates escalate as they have been recently or capture more gain when rates decline. Final thoughts One of the frustrations for yield oriented investors is there is no one place you can put your hard earned capital and earn high yields and have FDIC protection. However, I think it is also clear that there are a number of options that when mixed and matched could provide you with the overall yield you desire and enough diversity to potentially minimize losses if equity or bond markets decide to sell off. Let us know if we can help.  Right or wrong, depending on your view of the world, we are losing more and more rights everyday in a move towards bigger government in the United States and ultimately the bill for what that entails. The left calls this justice, the right socialism, but the fact is that the current progression will affect you in one way or another in the future no matter your income level.

We cannot continue to print money to hand out for entitlements and not have repercussions somewhere! The entitlements we do have, like Social Security, are already in trouble. Adding even more entitlements, such as Universal Basic Income (UBI), as so many want, will surely win votes, but will ultimately bankrupt our fine country. The greatest example of this slipper slope, we now find ourselves on as a country, is the Social Security Trust Fund, which is projected to be depleted by 2034. If you are like me, and getting older every day, those are funds you have factored into your retirement plans. What will we do if we no longer have a surplus from which to pay such payments to our nations retired? The answer is one of three not very palatable choices: 1) cut Social Security benefits by up to 25%, 2) raise taxes, or 3) inflate away the entitlement debt and the value of the Social Security you do get. My guess is that they will do all three when their backs are against the wall! How about the current proposed $3.5 trillion Infrastructure package? The Biden Administration has promised that this yet to be approved bill will have “zero cost.” The fact of the matter is it will have a cost. Nothing has a “zero cost” but instead taxes will have to be raised to offset or zero out these costs. Right on que, the House Ways and Means committee just that last week announced their plan to pay for the Infrastructure Bill. Here is their official list of possible tax increases on the table. What they plan is to tax the rich and effectively close some loopholes in the tax code to pay for most of this bill. Notice I said “most.” They could not even figure out how to get the entire $3.5 million needed without moving to on to the Average American for the rest of the dollars. They instead conveniently pretend the math will somehow work out! Higher Taxes for Everyone Let me tell you where this is going. The House Ways and Means Committee list of tax increases gives us a big hint. There is a tax that currently applies to net investment income (NIIT) under section 1411 of the Internal Revenue Code. The NIIT applies at a rate of 3.8% to certain net investment income of individuals, estates, and trusts that have adjusted gross income above $250,000 for married taxpayers filing jointly and $200,000 for single taxpayers. Now this tax initially was only on net investment income such as interest, dividends, royalty income, non-qualified annuities distributed earnings, and income from businesses trading financial instruments or commodities that are passive to the shareholder. It also includes capital gains such as the gain from the sales of stocks, mutual funds and bonds, distributions from mutual funds, the gain on the sale of investment real estate and also on the gain on the sale of partnership or corporate interests. The tax is fairly narrow and applies mostly to investment incomes. However, the House Ways and Means Committee is suggesting this tax be applied to all types of income for those about the income thresholds mentioned above. Do you see what just happened? They got us used to the tax and then expanded it. What happens next year or the year after when they are forced to deal with the Social Security Trust fund depletion? Will this tax, as an example, now apply to all income levels? The Time to Plan is Now So why do I mention this? Is it to get embroiled in a political discussion? Heck no! It’s to impress upon all our loyal readers and clients the urgency with which tax planning must now be part of your annual process if it is not already. Whether you are for the change or against it, someone has to pay for it! Margaret Thatcher famously said, “the problem with Socialism is that you eventually run out of other people’s money.” You may not agree that we are headed towards Socialism, but no one can deny that there is no such thing as a “zero cost” program. Someone must pay and that is going to be those with the ability to do so, no matter their income level ultimately! It will start with the rich, but believe me, it’s coming your way too. The solution is to be tax aware and to spend more time in the future arranging your affairs to minimize it’s drag on you and your family. This is not un-American; this is just smart planning! Some Ideas to Take Away As a start I want to give you three simple ideas that anyone can use to lower their tax burden:

Let me give you an example: In the past I had a client who sold out of his technical school for many millions of dollars. He contracted with an insurance company to purchase a private placement variable life solution and then used those dollars to pay a series of premiums to the insurer that included most of his funds from the sale. What he got for this was tax free account build up, the ability to borrow his funds back and the funds automatically pass to the next generation when he passed. The only thing missing in his planning was it was a part of his estate for estate tax purposes, at least the portion I managed as investment advisor. However, he would not have been able to borrow against the policy had he moved it out of his estate. So, this client, used this policy as his piggy bank. He borrowed from it when he needed funds and repaid policy loans when he had an excess of funds. Because all his money was in this policy, he had limited income annually and therefore paid little in taxes (and he lived in a very high tax state). He mitigated the single insurer risk by having more than one carrier underwrite the risk (it was shared). I could see more of this happening in the future as loopholes close and rates start to rise. The Bottom Line I believe taxes in this country are going to go up substantially in the years to come. This post is obviously not about tax evasion. Everyone should pay their fair share! However, there is also nothing wrong with arranging your affairs in such a way as to minimize what your fair share is and that is the point of this post. It is time to start thinking about it as I believe the forces of taxes, inflation and more will make it harder and harder for average Americans to make ends meet! This post is for educational purposes only. Please consult your tax professional before using any of the ideas presenting in this post. |