|

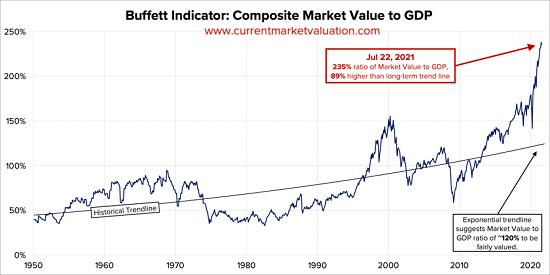

It’s the end of summer, what can I say. My vacation is upon me, I am tired and ready for some rest. The result is a Miscellany of short updates where my mind would not allow me to put together a well thought out blog post. Bad mind! Get some rest! High Yields on CashI know these to phrases no longer go together (high yields and cash). However, in our endless search for yield for clients, we did discover that the crypto space is paying yields up to 8.8% on stable coins, their version of cash. In today’s world that is a great yield!  From Celsius Yes, it is still a bit of the wild west, but one of my favorite Macro investors, Raoul Pal of Real Vision, believes the crypto space will increase by 500X over the next decade. If that is the case, can you really afford to ignore the space and the higher yields? We believe that the real opportunity here is for the blockchain leaders to pair with governments around the world to rollout digital versions of their currencies. We can already see this happening and believe in ten years; this space will be looked at like the internet is today, something we all take for granted but made some very wealthy. We can’t easily access crypto or the higher yields on traditional custody platforms today, but if this is something you would like to explore, let’s talk further about it? I have already done it myself. The Hoosier Football IndicatorIf there is any indicator I can think of that is pointing to the end of the world or at least a market crash it is the Hoosier Football Indicator. My beloved Hoosiers are ranked for the first time since 1969 in the AP pole. I said ranked, not rank. The latter is what they have been the last 50+ years.  If history is any guide, they will fall flat on their faces and underwhelm even their harshest critics. I also believe the fact that they are ranked must be some indication of a Bizzarro world, like on Seinfeld, where good is bad and bad is good. This can only mean negative things in my estimation for the markets and our economy. Run for the hills!! Markets Overpriced and Loving It!I have now been managing money for 27 years! Glad I started when I was 5 years old! The last twelve years have pretty much been like the weather here in Tampa, the same as yesterday and the day before. Hot with a chance of afternoon thunderstorms. There is a famous saying that many have uttered and that is “this time it is different.” Usually before they can finish with the last word of that phrase, they are proven wrong and the markets, economy or just about anything prove that “no – it is not different this time.” However, this time is different. You know why! If you said, all the asset purchases, stimulus, and spending bills. Give the man a dollar (now worth 1 cent in 1925 dollars due to inflation).  As you can see from the Buffet Indicator, market wise things are very, very and very expensive by historical standards, but where the government and the Fed are essentially the market, it can go as high as other nations will allow it before we lose the right to print our own currency (i.e., the right to be the reserve currency). We will lose this right someday, but for now roll them presses! By the way, it would be easy to get nervous about the markets, hide and never make the returns you should make. This is a great time to have an advisor as we typically have processes that keep us invested and you making money up until the bitter end when we all try to hit the exit at once. Woodlynne Farms Many of you probably did not realize that I am a farmer at heart. That is why it excites me that the long downward commodity cycle appears to be turning up.

It excites me so much I started a side-hustle growing microgreens in my oldest daughters’ bedroom. After all she is off to law school and does not plan to return except to visit! Check out this new venture at www.woodlynnefarms.com. For veggie haters, microgreens contain 5 to 40 times the nutrients of their larger full-grown cousins. This means you can eat less and still get your daily allowance of essential vitamins and nutrients. When I am back from vacation, if you live in Tampa and want to try a sample of Microgreens, just let me know.

0 Comments

Can you remember the time as a kid, or even with your kids today, that you purchased a container of bubble solution? The idea was simple, dip the applicator into the bottle, pull it out quickly and then blow into the applicator hole and watch the bubbles appear.  Oh, the joy of blowing bubbles and then watching them settle everywhere! Unfortunately, every bubble popped! It didn’t matter whether it was a little bubble, or the giant bubble produced by some kind of larger wand! They all popped! They either popped in air or popped hitting an object, like a blade of grass, but they all popped. It was just a matter of when, not if! The same can be said of economic bubbles, they all pop eventually. We saw the Dot.com bubble pop in 2000. The great recession bubble pop in 2007. Now it is just a matter of time until this one, “the mother of all bubbles,” pops. When it pops, watch out! I have written a lot over the years about this bubble! It has been a challenge for anyone but those willing to put their full faith in the Federal Reserve (the “Fed”) and “buy the dips.” The scary part is this is the only market many investment managers have ever seen. The type that goes up, never stays down, and that recovers almost instantaneously from any dips. In blogger Charles Hugh Smith’s recent Zero Hedge article entitled “The Moment Wall Street Has Been Waiting For: Retail Is All In”, he makes the case that this bubble has moved to a very dangerous stage, the “All-In” stage. This according to Mr. Smith is because up to this point, “the old hands on Wall Street have been wary of being bearish for one reason, and no, it's not the Federal Reserve, the old hands have been waiting for retail, the individual investor, to go all-in stocks. After thirteen long years, this moment has finally arrived: retail is all in.” He further makes the case that all you need to do is look at the investor sentiment, record margin debt levels and the Buffet Indicator (chart below) to see that we are at extremes. He makes the case that current valuations are “so extreme that the previous extreme in the 2000 dot-com bubble now looks modest in comparison.” Now Mr. Smith may have a point, but the critical thing about bubbles is they tend to go on much longer and go much further than most would ever imagine. Yes, we are thirteen years into this one, but does the Federal Reserve and our happily complicit officials in Washington have a choice, but to keep this one going through new spending programs, like the $1 trillion infrastructure bill now heading to the Senate, or the asset purchase programs in place by the Fed. In doing so, they are just blowing bigger and bigger bubbles. Ones that when they pop will hurt all but the nimblest of investors.

Charles Hugh Smith lists off a number of warning signs in his article that he believes to points to a possible crossroads for this current market bubble. Signs that are not new but happen at most tops. They include:

He wraps up the article by stating that these confident investors, the Robin Hood investors, do not realize one thing, they are “the marks and bag holders.” This market saga is not new! It happens over and over again, and Wall Street is a pro at drawing in retail investors who ultimately become overconfident, buy and hold or buy every dip, only to leave them holding the bag at the top of the market while they head for the exits. My friends, I would agree with Mr. Smith that we are approaching that proverbial “fork in the road” when markets top out and buying the dips no longer works. The question is not if, but like the bubbles you blew as a kid, when they pop! So how do I put a positive spin on this gloomy forecast? I would like to give you some simple ideas that might help you avoid holding the bag or being the bagman. They are not earthshattering, but they are tried and true!

Of course, we are here to help. If you would like to talk, just click here or give us a call. When I was just a young man, I would go with my dad to visit his mom (my grandmother). She was a very frugal, former school administrator, who lived in a duplex near our home. For whatever reason, the duplex did not have air conditioning and instead she would open all the windows and doors and run an old box fans during the summer months. I can remember getting bored with the adult conversation and I would sit in front of the fan to feel the cool breeze and hear the calming hum of the fan.  Like many a kid, I would eventually move to the backside of the fan and marvel at how the beating of the fan blades distorted the sounds of my voice. “Hello, hello, hello,” I would say. I would marvel at the way that the fan distorted my voice into a deeper, drawn out version of the original hello. The fan helped to circulate the air from one window and out another using cross ventilation. However, I can also remember hearing thunder clouds and lightning while there and my grandmother and father would quickly work to close many windows, some 100% and some less, but they heeded the warnings. Sometimes, we would be too slow to close the windows and doors or the storm would sneak up on us. When this happened, we would feverishly work as a team to close all the windows and doors to keep that rain from coming in the house. This process was a form of risk management. If we closed the window and doors, even if not entirely, we hoped to manage the possible risk of loss from water damage if the rain was able to blow into her duplex. Risk Management Today Similar to the risk management my grandmother displayed before a summer rainstorm, we as prudent money managers also must perform risk management. Like the approaching Indiana summer storm, we are really never sure how violent the storm will be, nor whether it will produce significant damage to the portfolio or not. However, much like closing doors and windows, it is better safe than sorry, even though a majority of storms produce very little in the way of damage. One of the things we do well as a firm is practice this risk management. Our average portfolio since 2003 has captured less upside over the years, just 88% of the benchmark’s upward movement. However, the big news is the same average portfolio has only captured 72% of the benchmark’s decline in percentage terms. We believe there is a time to open the windows and doors and turn the fans on high. In money management this is a new bull market or market move after an extended correction.  There is also a time to partially shut the windows and doors, so that a light rain does not damage the portfolio. This is where we move portfolios when we deem caution is warranted.

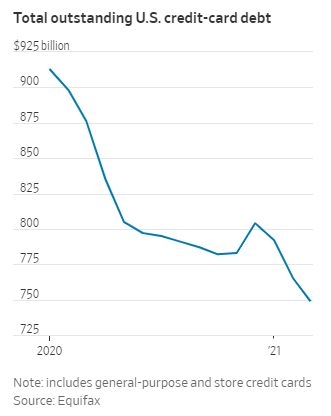

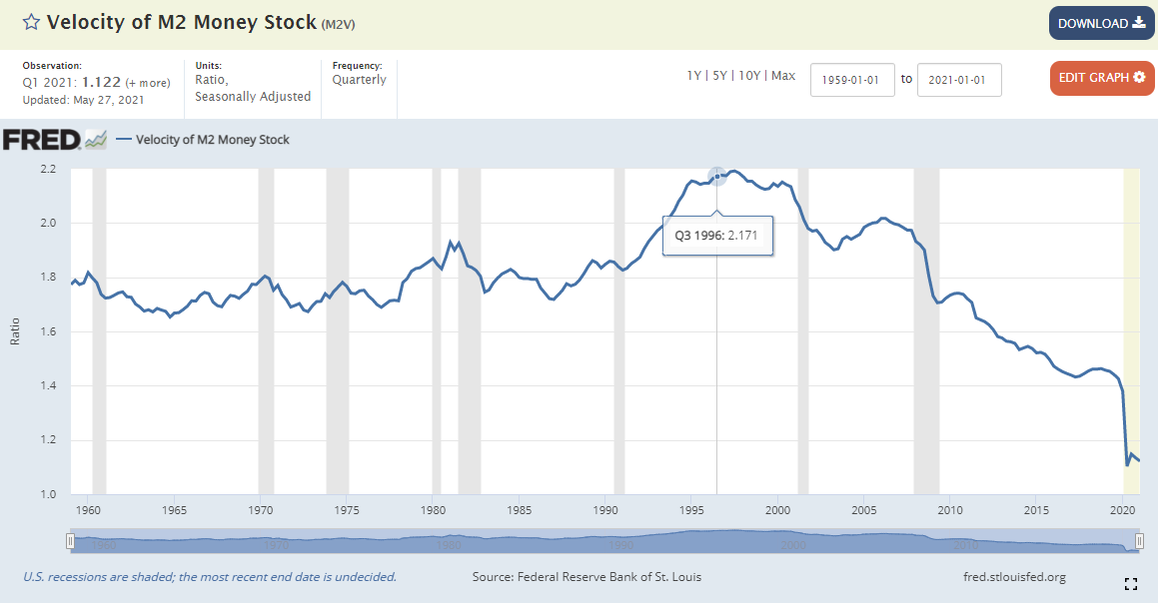

Finally, there is a time to shut all the windows and doors and if you are in Florida, to board them up, because the storm is going to be a big one and has the potential to create a lot of damage. This is when that caution turns into a major bear market, like we had in 2007-2008. History Says, Risk Management Pays Unfortunately, in the highly competitive, managed market we now find ourselves, too many managers have forgotten the risk management element or portfolio management. They will say “it doesn’t pay to manage risk, or the Fed has our backs.” You know what? They may be right in 9 out of 10 occurrences. However, it’s number 10 that defies the odds and creates long-term damage. After the longest bull market in history, you have to ask yourself, is this one the one out of ten. You know the occurrence that is different from the rest. We thought we had that in March of 2020, but quick intervention by the Federal Reserve and by Congress saved the day. Will they be able to save the day next time now that we are at even higher highs and have blown an even bigger bubble? As a student of history, all we need do is go back to the market declines of the 1920s and 30s to see what can happen after a market bubble. An investor that was fortunate enough to get out before those crashes, may have lost a little of their returns, but was quickly back to breakeven and then profits in the years that followed. The investor who rode down those markets spent the next 25 years wishing they had practiced better risk management! Only in 1954 did they finally get back to breakeven. Tell me that would not have fatally altered your retirement planning? I am not saying we are headed for a new depression, although it is possible. What I am saying is it only takes one “big one” to ruin everything you have saved a lifetime to grow. Think of it liking buying insurance. Sure, there is a cost to insurance, especially if you never need it. However, it provides peace of mind and even more if you ever need those funds. All it takes is one! So maybe my “hello, hello, hello” in the fan as a youth was really closer to the “hello McFly” from the movie Back to the Future? A wake-up call to those who continue to cheat fate and practice no or limited risk management, while the world blows bigger and bigger financial bubbles! Let us know if we can help! We are happy to offer a free second opinion on your portfolio. The Federal Reserve (“the Fed”) in each of its recent meeting releases has called the inflation we are now experiencing “transitory.” The result of the reopening of America post Covid-19 and supply chain disruptions with everyone attempting to purchase product all at once in a “just in time” inventory system that adjusted to the lack of demand in 2020 and now is having trouble getting back up to full capacity on the re-open. Our take is that the Fed is actually correct this time (as much as we hate to admit it). If there was lasting inflation in the economy, we would see it in the velocity of M-2 money, where money is changing hands from one person to another. As you can see in the St. Louis Fed chart below, the velocity of money is still trending lower.  If inflation was truly present, we would see rising use of credit. However, the Wall Street Journal reported on May 11th that “Americans are paying down their credit-card debt at levels not seen in years.”

Finally, is investment manager Kathy Woods of ARK investment Management. She says U.S. Set Up for 'Massive' Deflation! Our Take We believe the current inflationary trend is transitory. Much of it is supply chain related and purchasing managers have been ordering double or triple their normal order sizes to get product. Much of these orders will be cancelled when some product comes through the supply chain. We can already see Wall Street starting to move towards a slower growth and disinflationary stance in the charts as many commodity charts are now looking like they will correct (pull back) and technology and growth stocks appear to be bottoming.  For instance, this chart of the commodity CRB index shows that such prices are now at the historical downtrend line. The price momentum has waned and it starting to roll over.

In our portfolios, we have started to move away from pure commodity plays and back to deflationary assets, like precious metals as it is clear to us that the commodity complex will at least pull back here in a deflationary retreat. We believe that growth will come in slower than anticipated over the next few quarters on a comparative quarter over quarter basis. There will be more saber rattling about large tax increases by Washington and this will create a deflationary push back to growth stocks and away from value and commodities. Interest rates (i.e., yields) will again move sideways to down as it becomes clear that the inflation we have experienced, for the most part, was transitory. We believe you could see sideways to down markets in those names now doing well. We are not sure how far this weakness could extend, but it’s possible the whole market takes a breather. Weakening growth will spur further intervention by Washington and increased asset purchases by the Fed. This will help keep market stabilized and moving upward, but at what long-term impact? The next step we believe is that Americans and developed market consumers go back to life as normal. However, lurking out there some time down the road is the fact that consumers do become more confident and start spending. Maybe it because they finally start to make higher wages, which is inflationary. This spending begets spending and the velocity of money starts to turn upward. It is here where the Fed and other Central Banks now need to be careful as we could see not just inflation at that time, but hyperinflation because of a stimulus and easy money now prevalent in the markets. We obviously don’t know the timing of that latter phase, or if it will even happen. However, we do know that the market will continue to have periods of inflation and then deflation as it did in prior cycles. The easy money of the past 30-40 years is done, over. The same old 60% stock and 40% bond portfolio is going to struggle at times in this new cycle. So, let me leave you with a question? Is your advisor going to be able to navigate what I just laid out without losing you money? If the answer is “no,” how about scheduling a time to talk about your investment assets?  Courtesy NCAA.com - Fletcher Magee, one of the top ten three point shooters of the past decade. It’s March and that means basketball. This year is a bit odd in that the entire NCAA Men’s Basketball tournament is being played in Indiana and to make matters worse my alma mater, Indiana University, isn’t even in the tournament. However, a record nine Big Ten teams made the final 64 so all should be ok, right? Not exactly! Either these nine teams were grossly over rated, or the Big Ten teams had the worst seedings possible or both. Eight of the nine teams were beating in the first two rounds. Thankfully, Michigan came back to win against LSU, and we have at least one representative of the Big Ten in the final sixteen. Now folks that is embarrassing! So, in my embarrassment, not just for the Big Ten but for my now long-suffering Hoosiers, I set to work to figure out what was wrong with Big Ten Basketball. How could so many strong teams be eliminated so quickly? My unscientific conclusion after watching several games was that the Big Ten lacked 3-point shooters and was too focused on the inside 2-point game. Here is how the game has changed, according to Teamrankings.com, the average team shoots 37.7% from 3-point range while only 33.47% from 2-point range. Why on earth if those stat lines are true would you ever shoot a 2-point shot again? Now we know why? If all you shot was 3-point shots defenses would adjust and cut it off completely. However, the 3-point shot opens up the lanes and the middle of the court. This allows the centers and forwards to dominate inside at an even higher shooting average. One works to help the other! So, what does this have to do with wealth management? Answer – a lot! We have 3-point shots in finance that have better odds than shorter 2-point shots just like in NCAA Basketball. The clearest are the following:

I am sure this is just the tip of the iceberg as far as odds go, but their what come to mind immediately!

Let me know if you can think of any other 3-point shots in personal finances that defy the odds! |