|

Sometimes is seems the Federal Reserve and other Central Banks are running counterintelligence agencies and not reserve banks. A perfect example of this is Federal Reserve Chairperson Janet Yellen's comments on Friday that “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation,” the case for raising interest rates again has gotten pretty strong of late.

The truth is that the economy is weak and there is no way they are raising interest rates. This was evidenced by the market's fast intraday reversal of more than 100 Dow points. It seems the Fed's best tool at present is to talk the market into believing they are leaning towards interest rate normalization (i.e. tightening) and then find reasons not to follow through. At least the other Central Bankers are not so nefarious with their actions. They are out there buying equities and pumping up markets with ever increasing monetary stimulus. So where will all this lead? I spent a good part of the weekend trying to figure out just that. The truth finally hit me when I watched a simple economic video that defined deflation, hyperinflation and stagflation.

According to Crash Course, hyperinflation is where inflation rises by 50% or more per month. So with hyperinflation the velocity of money increases as people spend money as quickly as possible to avoid a decline in the value of their money. This increased velocity of money changing hands increases inflation exponentially.

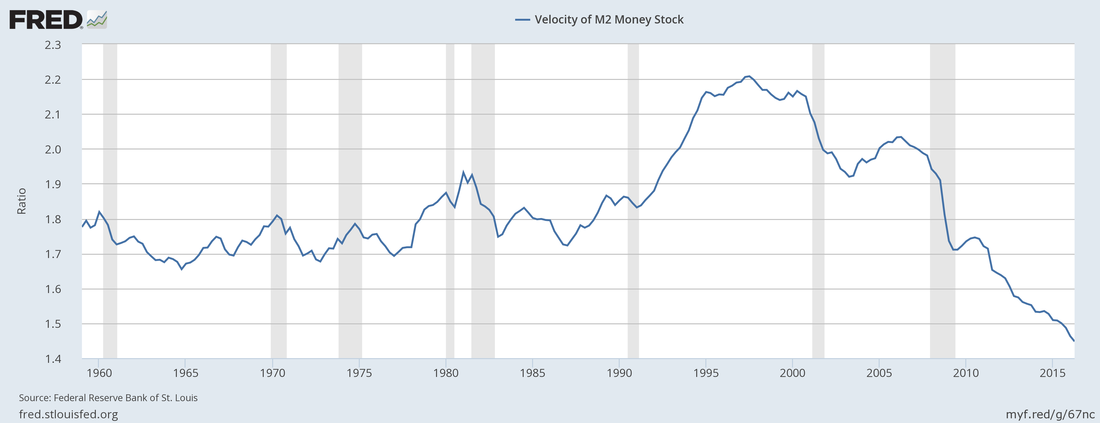

Deflation is a contraction in the supply of circulated money within an economy, and therefore the opposite of inflation results from declining or stagnate wages and falling prices. The velocity of money falls as people wait to buy what they perceive will be less expensive in the future. This decreased velocity of money changing hands increases deflation. Finally stagflation is when output stagnates at the same time that inflation rises. The end result of stagflation is price inflation, rising unemployment or stagnant wages and a disastrous economy. With stagflation the velocity of money may increase but output does not allow for significant increases as there is not the wage growth to support people spending money as quickly as it is earned. So the key to understanding where we are headed is to examine the velocity of money which luckily for us the St. Louis Fed provides to anyone who cares to look. Here is the current velocity of money:

M2 is a measure of the money supply that includes all elements of M1 as well as "near money." M1 includes cash and checking deposits, while near money refers to savings deposits, money market securities, mutual funds and other time deposits, according to Investopedia.com.

Notice how the velocity of money continues to fall off a cliff or move downward on the right edge of the chart. Assuming this data is accurate from the St. Louis Fed, this means that we continue to battle deflation. So as investors, what does this mean? First, you should delay buying things where prices have generally declined over time. The longer we wait, the lower the price (unless it is textbooks, college tuition, or healthcare).

Second, the government will not stop printing money until there is no more deflation and the velocity of money starts to rise.

This means that they will continue to try to find ways to make you feel wealthier, such as supporting equity markets. The Fed is not doing this directly, but Japan and Switzerland sure are buying U.S. equities and rumor has it that the U.S. has a facilities line with the Swiss that they are using to buying U.S. equities on behalf of the Fed because it cannot by mandate (at least openly). Mike Maloney of GoldSilver.com believes that first there will be deflation in the U.S. followed by all out monetary and fiscal assaults to overcome deflation and then that will be followed by hyperinflation. If he is right, we still appear to be in the deflationary stage and more stimulus is like to be the result. At the moment global growth is weak or in recession. The monetary policy is barely working because of wage stagnation, weak output and recessionary pains around the globe. All the more reason for those in power to double down! At some point, growth will increase and inflation will take off. So my final recommendation is use this time is to look for opportunities to buy at value today things that go up when inflation hits. These items include stocks, gold, real estate and other hard assets. I cannot tell you the timing of when things shift, but I believe it will happen. For all I know it may be happening now as gold has broken to new highs. I personally am looking to use the pullback currently underway to add to my position as a hedge against inflation and further debasement of global currencies.

3 Comments

I recently started binge watching AMC's Mad Men on Netflix after finishing all of season four of House of Cards in less than a week. Mad Men is set around the late 1950s and early 1960s and follows the rather torrid, high pressure lives of Madison Avenue advertising firms. The shows main character, Don Draper, in season one received a raise from his firm from $30,000 per year to $45,000.  Now being the boring financial type, my mind immediately wondered how inflation, or the increase in price levels, had affected Don's salary and what that would equate to in today's dollars. Fortunately, I did the math for you. The actual average inflation rate from 1960 - 2015 was 3.85% per annum according to the Bureau of Labor Statistics (BLS). If we assume his raise occurred in 1960, Mr. Draper's salary would be almost $360,000 in today's dollars. Now I have been to Manhattan many times and I can tell you that $360,000 does not go very far there now. However, my point is that inflation robs us of our purchasing power and governments love inflation and not so much its ugly cousin, deflation. Since governments love inflation, we must keep an eye on inflation. Fixed income or bond investors are the most at risk as their income stream is usually discounted by inflation to determine the value of today's money in the future. Inflation is what motivates equity investors to take risk in hope of higher returns. Where the bond investor is mostly just trying to protect capital and stay up with inflation after taxes, the equity investor is hoping that additional risk taking translates into additional returns up and above inflation and taxes. Of course as we have seen over the past decade or more there is no guarantee that this goal is achievable. So the bottom line here is that although Mr. Draper's theoretical salary may have risen, I would guess that Mr. Draper would tell you his salary today just "does not buy what it used too." As investors, we must realize that inflation can have a very real effect on our financial dreams and goals. We must work hard to position ourselves and our portfolios to at least stay up with the change in inflation. For those not yet in retirement, we must also realize that saving (or adding to our portfolios) tilts our chances of achieving those goals and dreams in our favor as depending on investment returns alone to outstrip inflation and taxes is not a game that everyone wins! By the way, April 15th is fast approaching! There is still time to add to your retirement savings and lower your 2015 taxes ahead of the April filing deadline. Let us know if we can help. |