Courtesy NCAA.com - Fletcher Magee, one of the top ten three point shooters of the past decade. It’s March and that means basketball. This year is a bit odd in that the entire NCAA Men’s Basketball tournament is being played in Indiana and to make matters worse my alma mater, Indiana University, isn’t even in the tournament. However, a record nine Big Ten teams made the final 64 so all should be ok, right? Not exactly! Either these nine teams were grossly over rated, or the Big Ten teams had the worst seedings possible or both. Eight of the nine teams were beating in the first two rounds. Thankfully, Michigan came back to win against LSU, and we have at least one representative of the Big Ten in the final sixteen. Now folks that is embarrassing! So, in my embarrassment, not just for the Big Ten but for my now long-suffering Hoosiers, I set to work to figure out what was wrong with Big Ten Basketball. How could so many strong teams be eliminated so quickly? My unscientific conclusion after watching several games was that the Big Ten lacked 3-point shooters and was too focused on the inside 2-point game. Here is how the game has changed, according to Teamrankings.com, the average team shoots 37.7% from 3-point range while only 33.47% from 2-point range. Why on earth if those stat lines are true would you ever shoot a 2-point shot again? Now we know why? If all you shot was 3-point shots defenses would adjust and cut it off completely. However, the 3-point shot opens up the lanes and the middle of the court. This allows the centers and forwards to dominate inside at an even higher shooting average. One works to help the other! So, what does this have to do with wealth management? Answer – a lot! We have 3-point shots in finance that have better odds than shorter 2-point shots just like in NCAA Basketball. The clearest are the following:

I am sure this is just the tip of the iceberg as far as odds go, but their what come to mind immediately!

Let me know if you can think of any other 3-point shots in personal finances that defy the odds!

0 Comments

(Tampa, FL) InTrust Advisors, Inc. is pleased to announce Keith Hruby, MSF, AAMS® as the newest member of our team.

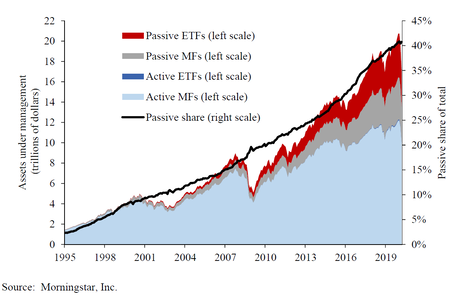

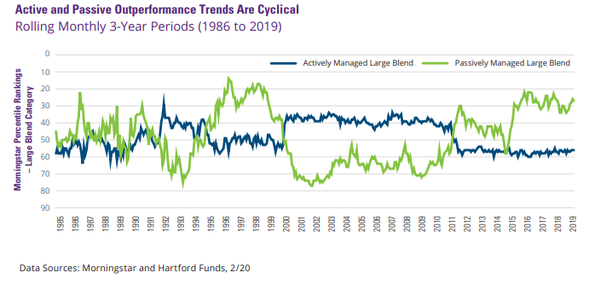

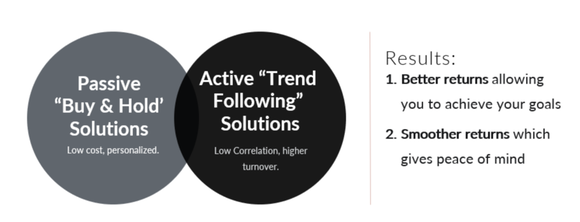

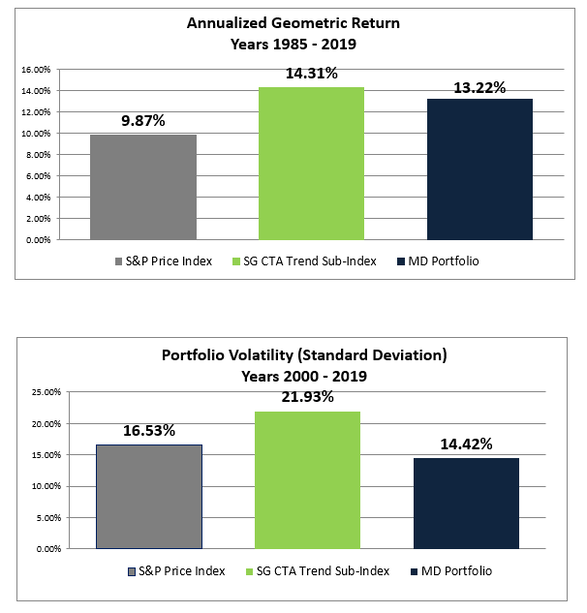

According to Jeff Diercks, the Founder and Managing Director of InTrust Advisors, "Keith brings valuable experience having served affluent families across the country. Keith brings a comprehensive understanding of tax and investment planning and how they relate to developing a holistic, effective financial plan." Mr. Diercks said further that "Keith has 10 years of experience working with affluent families and business owners providing specialized counseling in the areas of cash flow management, retirement planning, stock options and employee benefits, insurance, investments, income taxation and charitable planning." Keith began his career as a commissioned officer in nuclear submarines following his graduation from the United States Naval Academy. His military tours took him all over the world, including two deployments to the Western Pacific, a tour in Naples, Italy on the staff of the Commander, U.S. SIXTH Fleet, and a tour in Yokosuka, Japan on the staff of Commander, U.S. SEVENTH Fleet. He later was recalled to active duty to teach Finance and Economics at the U.S. Naval Academy, his Alma Mater. Keith was a Financial Advisor with Raymond James prior to joining InTrust Advisors. Keith’s unique skill set will enhance firm initiatives in helping clients maximize after-tax income through wise tax and investment planning. His passion is structuring charitable giving in order to minimize taxation of assets and maximize the impact to non-profit organizations. InTrust Advisors is a boutique multi-family office located in Tampa, Florida that works to remove the burden of planning and day-to-day management of complex tax, investment and estate structures for high net worth families nationally. As I mentioned in my previous post, when I first entered the business way back in 1995, it was quite common to look at portfolios and see a diverse set of assets including gold and silver, commodities, hedge funds and CTAs, as well as, equities and fixed income or bonds. Over the past ten to fifteen years however, the amount of market intervention by Central Banks and from global governments has made such diversification almost moot. Today, it’s much more common to see just portfolios of stocks and bonds. In fact, one of the greatest migrations we have seen is to portfolios that contain just passive index funds or ETFs. Part of this move has been due to cost, but the rest of the story is it has just not paid over the past 10 to 15 years to be in anything but the S&P 500 index. As the saying goes, “a rising tide lifts all boats” and the S&P 500 has been the broadest, lowest cost boat.  However as you know, tides don’t always rise and neither do stock and bond markets. We are already in the longest bull market on record for equities and bonds have enjoyed a thirty-year period of falling yields (rising prices) and there is just not much upside left with yields near the zero bound unless the Federal Reserve takes rates negative, which they have pledged not to do. As we noted in our post called “Is This the End of the Growth Cycle?”, eventually the growth cycle becomes corrupted by greed, fiat currency devaluations and debt expansion, which then replaces fundamentals (where we are today). As we saw in this same post, the solution is greater diversity of holdings to include precious metals, commodities, and volatility traders. Sounds simple enough but hold on there Kemosabe! It is not that easy! As we are seeing now, we may have continued Central Bank or Congressional intervention, which may prop markets up for periods of time. We have rolling bouts of deflation, with inflation in some areas. Eventually deflation may give way to inflation. This is a process and it is fluid! Enter the active manager, no longer the goat of the past 15 years, this guy may add a great deal of value going forward. By goat I do not mean the Tom Brady type of goat (Greatest of All Time). I mean the type that eats your schoolwork or craps on your floor if you bring it in from the field. The bad type! In our opinion, the days of buying and holding the S&P 500 Index are drawing to a close. This doesn’t mean low cost index funds do not make sense. It just means that days of buying and holding through thick or thin are probably drawing to a close. Volatility is on the rise and it has remained elevated as you can see here from this weekly graph of the VIX or volatility index. This means more heart burn generally and much less stability in stock and bond prices.  With volatility elevated, this is the time that active management shines. The active manager is first and foremost a risk manager. He presses the gas petal when conditions are right. He stomps on the brake petal when conditions change. He may even raise his foot some and take some pressure off the gas petal in our proverbial car when conditions are starting to look dicey. History also shows that outperformance tends to be cyclical. With the latest period of passive outperformance, here in large capitalization stocks, now approaching a decade, it may be time to assume this equation will flip again.  We believe the perfect portfolio solution is a mix of the passive buy and hold and the actively managed. We call this mixture a multi-disciplined portfolio.  Here you can see those expected results when comparing the SG CTA trend follower sub-index with the S&P 500 index and then a 50%/50% multi-disciplinary portfolio for both indexes.  Notice how returns were better and volatility risk (standard deviation) was lowered in the process.

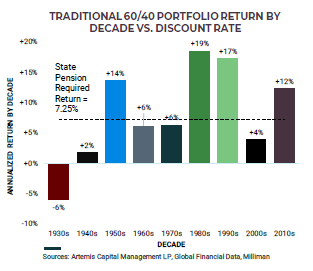

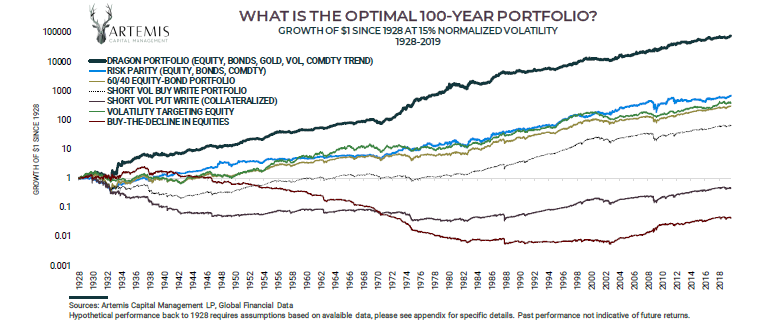

This is obviously a simplified model and depending on your portfolio size and your financial goals, this portfolio may include active investment strategies like several we run, passive buy and hold portfolios (which we also run), hedge funds, commodity trend followers (many times known as CTAs), precious metals, bitcoin and more. Since very few of us have a crystal ball, let alone one that works, the portfolio diversity is increased to handle an environment that is more fluid and volatile. Let us know if this is something, we can explore for you?  When I first entered the business way back in 1995, it was quite common to look at portfolios and see a diverse set of assets including precious metals, commodities, hedge funds and CTAs, as well as, equities and fixed income or bonds. Over the past ten to fifteen years however, the amount of market intervention by Central Banks and from global governments has made such diversification almost mute. Today, it’s much more common to see just portfolios of stocks and bonds. Investments in precious metals, commodities, hedge funds and CTAs (for the most part) have been underperformers. A loser’s game! I mean had we all known then what we know today, we would have all just bought the S&P 500 index right? We would have learned to deal with the market volatility knowing that each market decline would spawn a reaction by global central banks and governments to prop back up the ailing markets. However, as we all know hindsight is 20/20! I still marvel at why such parties cannot let the markets do what they do best, i.e. run in cycles of boom and bust. The busts bring sanity to the markets and help to eliminate the bad players. They have to realize that when this managed market does end, it is going to end very badly for many participants, or maybe that is the plan? Who knows? My point is that a portfolio today that includes 60% equities and 40% bonds is not really diversified when stocks are at nosebleed valuations and bonds are at historical thirty-year lows in yields and near zero yields. The protection that bonds now afford investors to hedge equity volatility is muted at best if not non-existent. I can actually envision a scenario where both stocks decline, and bond yields rise, and investors lose money on both sides of the portfolio at once. So, what is an investor to do? Since markets are mean reverting, I believe we need to start to look to the past to move forward into the future. This means a slow reversion back to portfolios that are more diversified and contain assets classes that have historically provided some shelter in the storm, whether that is equity market volatility, rising deflation or inflation, currency devaluations and more. In a study that Artemis Capital Management performed in January 2020, they found that over the past 100 years it was common to have periods like we have had whereby growth reigns fueled by the virtuous cycle of value creation and rising asset prices. The growth cycle began naturally through a combination of favorable demographics, technology, globalization and economic prosperity. However, such growth eventually became corrupted by greed. Fiat currency devaluations and debt expansion replace fundamentals. Isn’t that exactly where we are today? Those growth periods were followed by periods where the corrupted growth cycle was destroyed. This destruction led to a periods of either deflation or inflation, many times alternating from one to the other. The deflationary path was caused by an aging population which leads to low inflation, faltering growth, financial crashes and then debt defaults. The inflation cycles were led by fiat currency defaults, and helicopter money. Maybe you recognize the helicopter money as the latest $600 stimulus checks just approved by the Congress? During these latter periods of corrupted growth and intermittent periods of deflation and inflation, they found that traditional portfolios of 60% equities and 40% bonds underperformed. What they found is that more diversified portfolios that included commodity trend followers, precious metals and volatility traders significantly outperformed the latter 60%/40% portfolios during these periods.  We believe we are in the latter stages of that corrupted growth cycle.

The transition has to start now to more diversified portfolios that include more than just equities and bonds. To more of the diversified portfolio like you see above that Artemis has called the Dragon Portfolio. We will write on this later, but we also believe that means a renewed importance of having both passive index strategies and active investment strategies in your portfolio, a multi-disciplined portfolio as we call it. Just like the latest fashions, what is old is new and what is new is old. Funny how that works! So, the question becomes “what’s in your portfolio?” If this is not a discussion you are having with your advisor, it may be time to find a new advisor? Let us know if we can help. Just a few weeks ago, the headline risk was all negative. The narrative was that Covid-19 was spreading throughout the world in a second wave. Countries were closing down again. Would the U.S. be next to close down like in early 2020 and it was rumored this would most likely happen with a Biden win?  Speaking of the Presidential Election, the main-stream media did a pretty good job of fear mongering regarding that election. What if Trump won? Would there be rioting in the streets and general unrest? The narrative went that such unrest could be very negative for your portfolio and for America! Turns out the Trump has not won (at least not yet as he pursues legal action in various swing states). Instead, Joe Biden appears to be the overwhelming favorite to assume the role of President come January. Then recently, Pfizer announces a possible vaccine for Covid-19 with 90% effectiveness. Stocks of course are rallying like there is no tomorrow on the news and breaking to fresh highs clearing technical hurdles that just a few days ago we thought might lead to a market reversal. The cynic in me wonders if Pfizer had a possible vaccine prior to the election but waited until Biden’s win to announce the trial effectiveness, but I digress. Maybe it’s just me, but it seems the good news is now coming in batches. No matter the reason, my point here is that the market will do what it wants. It is an untamed animal that requires it be followed, not forecast. Why Forecasting Doesn’t Work? Have you noticed how many guests on CNBC are clamoring to give their market forecast? The reason is that it cost them nothing to do so, but if they are lucky enough to get it right, it could change their standing forever. As I think back over time, I can remember a CNBC guest named Elaine Garzarelli. She was credited with calling the bottom of the 1982 and 1984 Bear Markets and the top of the 2000 Bull Market. However, where is she today? I don’t even know. You rarely see her anymore on any news channel. I can tell you it’s pretty hard to get the calls consistently right or we would hear more from or about her. The constant flow of news and changing market conditions is what makes forecasting markets so tough. As an example, we have been using a service called Hedgeye to provide us fundamental data on global economies and the markets. The founder of this group is a pretty brash guy named Keith McCullough. He and his group are constantly updating their subscribers on the economic quad that they believe the data is telling them that we are entering. Mr. McCullough bad mouths the Old Wall and investors who see the markets differently.  However, like Elaine Garzarelli before him, the constant change in the market narrative, the amount of market control now exercised by global Central Banks and the monetary policy (stimulus) that governments keep implementing has made their forecasts all but worthless. We recently cancelled our agreement with them as a result. The Key to Success We continue to believe the key to success is to follow the market until it tells you the trend is reversing. We call this Trend Following and it is something that is built into every portfolio we run.  It is not perfect, and we usually give up some upside and give back some profits waiting on the signals. However, it is a discipline and allows us to stay focused on the trend and not the short-term noise.

We like it for a number of reasons:

This latter point I believe is one of the most important. When the election approached, our models had us reduce exposure, which is good money management. However, those same models did not have us out of the market. Now that the market is rallying again, we are participating in the rally and not sitting on the sidelines. Had some of the doom and gloom occurred that we mentioned previously, we would have limited downside risk. We may now be underperforming on the upside as we look for the right time to possibly add back some exposure, but we did what our clients pay us to do and that is to “manage risk” first and foremost and generate positive returns as a secondary goal. Maybe our process could help you? If so, please click here for a free consultation. |