|

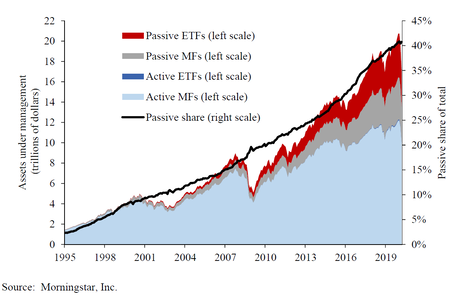

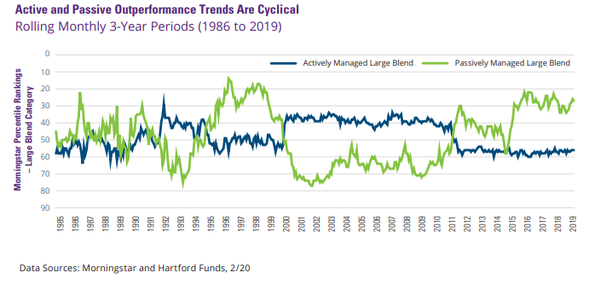

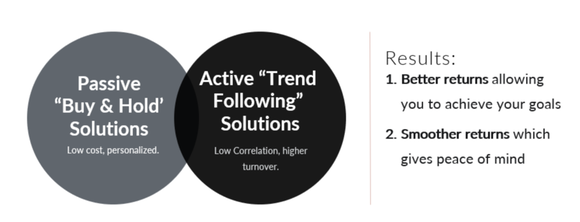

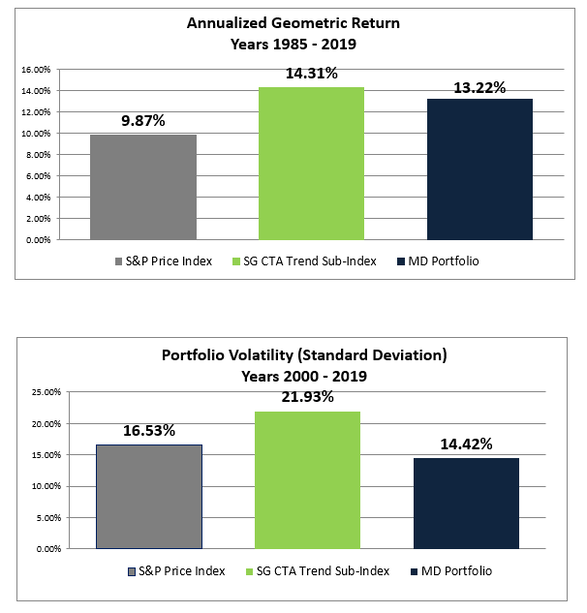

As I mentioned in my previous post, when I first entered the business way back in 1995, it was quite common to look at portfolios and see a diverse set of assets including gold and silver, commodities, hedge funds and CTAs, as well as, equities and fixed income or bonds. Over the past ten to fifteen years however, the amount of market intervention by Central Banks and from global governments has made such diversification almost moot. Today, it’s much more common to see just portfolios of stocks and bonds. In fact, one of the greatest migrations we have seen is to portfolios that contain just passive index funds or ETFs. Part of this move has been due to cost, but the rest of the story is it has just not paid over the past 10 to 15 years to be in anything but the S&P 500 index. As the saying goes, “a rising tide lifts all boats” and the S&P 500 has been the broadest, lowest cost boat.  However as you know, tides don’t always rise and neither do stock and bond markets. We are already in the longest bull market on record for equities and bonds have enjoyed a thirty-year period of falling yields (rising prices) and there is just not much upside left with yields near the zero bound unless the Federal Reserve takes rates negative, which they have pledged not to do. As we noted in our post called “Is This the End of the Growth Cycle?”, eventually the growth cycle becomes corrupted by greed, fiat currency devaluations and debt expansion, which then replaces fundamentals (where we are today). As we saw in this same post, the solution is greater diversity of holdings to include precious metals, commodities, and volatility traders. Sounds simple enough but hold on there Kemosabe! It is not that easy! As we are seeing now, we may have continued Central Bank or Congressional intervention, which may prop markets up for periods of time. We have rolling bouts of deflation, with inflation in some areas. Eventually deflation may give way to inflation. This is a process and it is fluid! Enter the active manager, no longer the goat of the past 15 years, this guy may add a great deal of value going forward. By goat I do not mean the Tom Brady type of goat (Greatest of All Time). I mean the type that eats your schoolwork or craps on your floor if you bring it in from the field. The bad type! In our opinion, the days of buying and holding the S&P 500 Index are drawing to a close. This doesn’t mean low cost index funds do not make sense. It just means that days of buying and holding through thick or thin are probably drawing to a close. Volatility is on the rise and it has remained elevated as you can see here from this weekly graph of the VIX or volatility index. This means more heart burn generally and much less stability in stock and bond prices.  With volatility elevated, this is the time that active management shines. The active manager is first and foremost a risk manager. He presses the gas petal when conditions are right. He stomps on the brake petal when conditions change. He may even raise his foot some and take some pressure off the gas petal in our proverbial car when conditions are starting to look dicey. History also shows that outperformance tends to be cyclical. With the latest period of passive outperformance, here in large capitalization stocks, now approaching a decade, it may be time to assume this equation will flip again.  We believe the perfect portfolio solution is a mix of the passive buy and hold and the actively managed. We call this mixture a multi-disciplined portfolio.  Here you can see those expected results when comparing the SG CTA trend follower sub-index with the S&P 500 index and then a 50%/50% multi-disciplinary portfolio for both indexes.  Notice how returns were better and volatility risk (standard deviation) was lowered in the process.

This is obviously a simplified model and depending on your portfolio size and your financial goals, this portfolio may include active investment strategies like several we run, passive buy and hold portfolios (which we also run), hedge funds, commodity trend followers (many times known as CTAs), precious metals, bitcoin and more. Since very few of us have a crystal ball, let alone one that works, the portfolio diversity is increased to handle an environment that is more fluid and volatile. Let us know if this is something, we can explore for you?

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |